Abstract

The report provides a comprehensive exploration of the emergence, growth, and future prospects of sim racing in India, offering a nuanced understanding of this evolving niche within the gaming and esports industry. Beginning with a historical overview, it traces the origins of sim racing in India and its gradual integration into the broader gaming culture. Key milestones are highlighted, showcasing how sim racing transitioned from a niche activity to gaining recognition as a legitimate form of competitive gaming. The report further examines the transformation of sim racing from a casual hobby into a professional esport, driven by the rise of online tournaments, the professionalization of gaming, and increased participation from Indian players. The influence of global trends, such as international events, technological advancements, and the involvement of global esports organizations, is also analyzed, demonstrating their significant role in shaping and elevating the Indian sim racing ecosystem.

A critical component of the report focuses on the infrastructure and ecosystem development within the country. It delves into the accessibility of sim racing hardware and software, discussing the affordability and availability of gaming equipment through both local and international manufacturers. Additionally, the role of gaming communities and esports organizations is explored, emphasizing their contributions in establishing leagues, fostering collaborations with global entities, and driving community-led initiatives. The involvement of Indian motorsport organizations and automotive manufacturers is also highlighted as a crucial factor in supporting the growth of sim racing through investments, technological innovations, and partnerships.

The report identifies the increasing popularity of sim racing among Indian gamers and motorsport enthusiasts, attributing this growth to shifting demographic trends, changing gaming preferences, and cultural factors. However, it does not overlook the challenges that hinder wider adoption, such as the high cost of equipment, limited awareness, and accessibility barriers. Initiatives aimed at overcoming these obstacles are discussed, providing insights into efforts to make sim racing more inclusive. Looking ahead, the report emphasizes the significant potential for growth in India’s sim racing ecosystem, particularly through the expansion of esports tournaments, sponsorship opportunities, and the establishment of training platforms. Strategies to create a sustainable competitive environment are also explored, with a focus on fostering long-term engagement.

Overall, the report presents a detailed and structured analysis of sim racing in India, offering valuable insights into its historical evolution, current ecosystem, and future opportunities. By integrating perspectives on infrastructure, community development, global influences, and adoption challenges, it provides a holistic understanding of the factors driving the rise of sim racing in the country.

Evolution and Growth of Sim Racing in India

Historical Overview and Entry into Indian Gaming Culture

The evolution of sim racing in India represents a unique intersection of technological proliferation, the gradual maturation of motorsport culture, and the explosive growth of the broader gaming ecosystem. As of February 2026, the trajectory of this discipline can be mapped through a timeline of roots and entry, developmental milestones, and an ongoing phase of mainstream integration, as visualized in the industry’s historical analysis. The history of sim racing in India has not been thoroughly documented or explored in the available sources, and much of the information provided is either outdated or tangential, yet distinct patterns emerge when analyzing the broader gaming landscape alongside specific sanctioned events[5]. The narrative of sim racing is not one of sudden ubiquity but rather a sporadic development, where the virtual track has slowly gained legitimacy alongside efforts to revive traditional physical motorsports.

Tracing the roots and initial entry of sim racing into Indian gaming culture requires an understanding of the broader digital environment that facilitated its arrival. The Indian gaming market, which has now expanded to a value of 3.7 to over 4 billion USD, serves as the foundational bedrock for niche sectors like sim racing to take hold[1]. The entry phase was characterized by a fragmented community of enthusiasts, largely separated from the mainstream gaming narrative which was dominated by mobile-first titles. However, the democratization of technology acted as a catalyst. The rapid growth of the gaming sector has been driven by factors such as widespread smartphone adoption, expanding 5G coverage, and the convenience of Unified Payments Interface (UPI) payments, which have collectively made high-fidelity gaming experiences more accessible and integrated into daily life[1][4]. While sim racing is traditionally associated with high-end PC hardware and dedicated rigs, the inclusion of both PC and console racers in emerging events highlights a strategic attempt to broaden accessibility and inclusion within this field. This accessibility is critical, as it bridges the gap between casual arcade racing and the rigorous simulation required for competitive esports.

As the narrative moves from initial roots to developmental milestones, the role of institutional sanctioning bodies becomes pivotal. A significant marker in the evolution of Indian sim racing was the establishment of events such as the National Esports GT3 Championship. According to promotional materials, the Federation of Motor Sports Clubs of India (FMSCI) sanctioned this event, suggesting distinct efforts to formalize competitive sim racing in the country. This sanctioning is a crucial developmental milestone, as it lends credibility to the discipline, elevating it from a hobbyist pursuit to a recognized sport under the aegis of the national motorsport federation. However, the temporal context of these initial formalization efforts remains somewhat unclear, and the lack of longitudinal analyses leaves gaps in understanding the precise sequential growth of these leagues[5]. Nevertheless, the dominance of discussions regarding physical motorsports provides essential context for the environment in which sim racing is developing. Recent reports from early 2024 and continuing into February 2026 indicate a robust interest in bringing traditional motorsports back to India, such as the government’s exploration of hosting Formula 1 races[3]. While these plans are linked more to live motorsport than sim racing, the resurgence of automotive culture creates a symbiotic ecosystem where virtual racing can thrive as a pathway or parallel discipline.

The integration of sim racing into the mainstream gaming ecosystem is further influenced by the government’s strategic outlook on the creative economy. The 2026 Union Budget underscores a deepening commitment to nurturing the gaming and creative industries, with initiatives like the push for Animation, Visual Effects, Gaming, and Comics (AVGC) labs and National Creator Labs supported by a 250 crore Indian Rupee allocation[3]. This level of institutional investment aims to foster innovation, skill development, and professional careers, potentially shaping the future trajectory of specialized gaming sectors like sim racing[5]. Sim racing relies heavily on physics simulation, graphical fidelity, and broadcasting technology—all areas that benefit directly from a robust AVGC sector. Consequently, the government’s focus on building a robust ecosystem for creative and gaming enterprises highlights a deeper institutional recognition of these sectors’ economic and cultural significance. This creates a fertile ground where sim racing can transition from a niche activity to a viable career path for developers, competitive drivers, and content creators.

Despite these advancements, the integration of sim racing into the broader cultural fabric of Indian motorsport remains a complex process. The 2026 “Generation Speed” motoring festival, scheduled for February 7th and 8th at Aamby Valley, signifies a palpable enthusiasm for automotive culture but fails to explicitly mention sim racing in its programming or historical context[4]. This omission suggests that while automotive passion is high, the complete convergence of the physical and virtual racing worlds is still underway. Similarly, reports emphasizing the Indian government’s push to revive Formula 1 often address physical motorsports without explicitly addressing sim racing, indicating a continued focus on traditional racing developments over virtual ones[2]. However, the scattered nature of these sources does not diminish the growing cultural footprint of gaming. Indian esports, once primarily competition-focused, is transitioning toward becoming an embedded cultural element, and the broader popularity of online multiplayer setups reflects evolving gaming habits where casual gamers transform into paying participants[2][4]. This shift in consumer behavior is vital for sim racing, which requires investment in hardware and software.

The evolution of sim racing in India is therefore best understood as a component of the larger “Mainstream Integration” of gaming in the country. The market, supported by 400 to 500 million gamers, has reached a critical mass where sub-genres can sustain dedicated communities. The blurring of lines between gaming and other creative fields, such as content creation, further supports this integration. The growing infrastructure for animation and game design, coupled with increasing opportunities for creators, is indicative of the ongoing maturation of the industry[1]. As of February 2026, without dedicated sources mapping sim racing history in India comprehensively, the available data remains anecdotal; however, the sanctioning of esports events like the National Esports GT3 Championship and the overarching growth of the AVGC sector provide strong evidence of a discipline that is steadily carving out its historical chapter[3].

In conclusion, the growth of sim racing in India has been shaped by a combination of technological advancements, government policies, and changing consumer behaviors. From its undocumented roots to the sporadic yet significant milestones of FMSCI-sanctioned events, the discipline is navigating a path toward mainstream acceptance. While physical motorsport events like Formula 1 bids and motoring festivals dominate the headlines, the underlying digital infrastructure—boosted by 5G, UPI, and government skilling programs—is laying a durable foundation for virtual racing[2]. The period around February 2026 reflects significant momentum, where the investments in technology and skills are transforming sim racing from a peripheral activity into a recognized facet of India’s evolving sports and gaming landscape.

| Stage of Evolution | Key Characteristics |

| Roots and Entry | Tracing the origins and initial entry of sim racing into the Indian gaming culture |

| Developmental Milestones | Occurrence of key events and milestones highlighting industry growth |

| Mainstream Integration | Gradual integration of sim racing into the broader mainstream gaming ecosystem |

Transition from Hobby to Competitive Esport

The trajectory of sim racing in India represents a distinct paradigm shift within the broader electronic sports ecosystem, characterized by a rapid evolution from a fragmented leisure activity to a structured competitive discipline. This transition is not merely a reflection of changing consumer preferences but is deeply intertwined with the maturation of the Indian gaming industry, government policy interventions, and the global convergence of digital and physical motorsports. As of February 2026, the landscape of sim racing in India is defined by significant quantitative growth in participation and a qualitative shift toward professionalization, although the sector continues to navigate infrastructure challenges and the need for region-specific developmental frameworks.

To understand the magnitude of this transition, one must examine the participation metrics that underscore the rising popularity of the genre. Data tracking the estimated growth of competitive sim racing participants in India between 2019 and 2024 reveals a stark upward trend, indicative of a burgeoning market. in 2019, the ecosystem was undeniably niche, recording a minimum value of approximately 800 active competitive participants. This figure represented a foundational community, likely comprised of enthusiasts operating in isolation or small, informal groups. However, over the subsequent five-year period, the sector witnessed an exponential expansion. By 2024, the number of active competitive participants had surged to reach a maximum value of 32,000. This drastic increase signifies more than just added volume; it suggests a fundamental transition in how the Indian gaming demographic perceives racing simulation—moving from casual play to active engagement in competitive structures. While this data creates a compelling narrative of growth, it is worth noting that specific, updated data on the competitive development of sim racing in India beyond this period remains sparse as of early 2026.

The impetus for this transition is multifaceted, driven heavily by macro-level shifts in the Indian gaming industry’s regulatory and economic environment. A pivotal moment in this professionalization journey was the nationwide ban on real-money gaming (RMG) enacted in 2025, coupled with the introduction of a 40% tax on certain gaming revenues. These legislative measures fundamentally reshaped the gaming landscape by redirecting investment capital and player interest away from chance-based applications and toward skill-based esports. Sim racing, being inherently skill-dependent and devoid of gambling mechanics, emerged as a beneficiary of this ecosystem redistribution. This shift contributed to a more structured environment for professional esports, signaling a definitive move away from less regulated gaming practices and lending greater legitimacy to competitive genres[14]. Consequently, the transition from hobbyist to professional aspirant has been accelerated by a regulatory framework that prioritizes the integrity of skill-based competition.

Furthermore, the government’s recognition of the gaming sector as a vital economic engine has provided a conducive atmosphere for the growth of niche esports like sim racing. As of February 2026, there is a clear and intensified focus on advancing the industry, evidenced by the provisions in the Union Budget 2026-27[12][15]. This budget allocates substantial resources to the Animation, Visual Effects, Gaming, and Comics (AVGC) sector, aiming to strengthen the “Orange Economy,” which encompasses creative industries[12]. These developments mark a strategic move to address the increasing demand for a trained workforce and establish a more professional ecosystem for gaming in India[15]. For sim racing, which relies heavily on high-fidelity graphics, physics engines, and simulation hardware, the government’s push for talent development through skilling programs creates a robust backend infrastructure. The emphasis on skilling is a forward-looking initiative that supports not just the players, but the developers, engineers, and tournament organizers required to sustain a professional league structure.

Despite these positive indicators, the transition to a fully realized professional esport is not without hurdles. Global observations from late 2023 noted that competitive sim racing struggled with mass appeal due to limited efforts to expand its audience, a challenge that likely persists within the Indian context given the absence of region-specific insights to the contrary[13]. While sim racing is steadily gaining credibility as it converges with traditional sports and creates opportunities for innovation, the lack of India-specific data limits the assessment of how effectively these global trends are being localized. In early 2026, sim racing is noted to have shifted from a niche segment to gaining wider recognition globally, involving stakeholders like teams and developers, yet there is no in-depth discussion of India’s dedicated competitive esports leagues in current reports. This suggests that while the participant base has expanded to 32,000 as of 2024, the commercial and spectator infrastructure—key components of professionalization—may still be in a developmental phase relative to established esports titles.

The economic reality for aspiring professional sim racers in India also reflects a transitional state. Streaming revenues continue to drive individual gamer incomes, making live-streaming a viable career path alongside competitive play. However, concerns regarding income stability and long-term career sustainability persist, highlighting areas where the industry still needs to mature to support full-time professionals exclusively through competition winnings or team salaries[11]. While industry predictions from 2022 suggested ambitious goals for the AVGC sector to become a massive economic contributor by 2026 with substantial job creation, the realization of these figures specifically for the sim racing niche requires critical assessment in the current timeframe[13]. Nevertheless, government efforts to support content creators align with these economic projections, signaling a recognition of gaming’s potential as a significant economic contributor.

The integration of competitive esports within the racing simulator market remains a key global trend, with increasing adoption by professional motorsports teams and leagues. This convergence offers a unique pathway for Indian sim racers, potentially bridging the gap between virtual competition and real-world motorsport, a trajectory less available to other esports genres. However, earlier esports predictions emphasizing regionalized formats and localized tournaments did not delve into India’s specific genre dynamics, leaving a gap in understanding how Indian organizers are capitalizing on this potential[12]. While India remains an emerging market with rapid technological adoption and an expanding esports base, there is limited direct evidence pointing to a fully-developed competitive sim racing infrastructure in the country as of the analyzed sources[11].

In conclusion, the evolution of sim racing in India from a hobby to a competitive esport is marked by substantial quantitative growth and a supportive, if evolving, regulatory environment. The surge in active participants from 800 in 2019 to 32,000 in 2024 provides empirical evidence of the sector’s expanding footprint. This growth is underpinned by the professionalization of the wider Indian gaming industry, driven by the Union Budget 2026-27’s focus on the AVGC sector and the strategic pivoting caused by the 2025 RMG ban[14][15]. However, the ecosystem remains a work in progress, influenced by evolving policies and market dynamics, and faces persistent challenges regarding mass audience appeal and long-term career stability for competitors[11][13][14]. Thus, while the foundation for a professional sim racing industry in India has been laid, the transition is ongoing, requiring further infrastructural development to match the enthusiasm of its growing participant base.

Influence of Global Trends on the Indian Sim Racing Scene

As of February 2026, the evolution of sim racing in India is increasingly defined by its integration into the broader global esports ecosystem, characterized by a symbiotic relationship between international technological trends and domestic structural reforms. The Indian market, traditionally viewed as a burgeoning sector, has begun to mirror the sophisticated trajectories observed in established global regions, primarily driven by rapid technological innovation and significant shifts in governance and policy. The landscape of global sim racing reflects key trends and technological advancements that are significantly influencing markets worldwide, including India, creating a ripple effect that reshapes how Indian enthusiasts and professionals engage with the sport.

One of the most profound global influences on the Indian scene is the acceleration of hardware and software fidelity. Historical data from early 2024 predicted that the global sim racing hardware market would witness substantial growth by 2030, driven by sustainable practices and technological innovation[21]. By February 2026, these projections have materialized into tangible market realities, where the availability of advanced peripherals—such as direct-drive wheelbases and load-cell pedals—has become a defining metric of the Indian sim racing standard. While specific Indian adoption rates remain inferred, the global surge in hardware accessibility has undeniably modernized Indian racing practices. Recent developments in early 2026, described as huge changes in the sim racing domain, point toward fresh innovations in hardware and heightened esports competitiveness, which are expected to have cascading effects on the Indian market. These advancements are not merely cosmetic; they fundamentally alter the training methodologies of Indian drivers. The increasing application of high-fidelity simulators in sports supports the integration of advanced training tools in sim racing, potentially fostering a new generation of professional racers in India who can transition between virtual circuits and real-world tracks with greater fluidity[24].

The alignment of India with global standards is further catalyzed by significant policy shifts that occurred in early 2026. The intersection of general esports governance and specific sim racing activities has become a focal point for industry growth. The period surrounding the 2026 Union Budget was critical, as anticipations highlighted the gaming and esports industry’s hopes for formal government support to elevate its global standing[21]. This expectation for streamlined regulations and investment incentives was met with a historic milestone when Esports was officially recognized as a sport in India. This recognition is expected to catalyze substantial development in the industry, laying a foundation for structured investments, talent nurturing, and global partnerships, which are essential for international integration[15]. For the sim racing community, this official status is transformative. It legitimizes the pursuit of virtual racing as a professional career rather than a recreational pastime, thereby attracting institutional sponsors who were previously hesitant due to regulatory ambiguity.

The influence of global organizational structures is also evident in the way Indian teams are now managed and commercialized. As indicated by the comparison of global trends and the Indian ecosystem, the dominance of mature global esports entities has directly influenced the formation and management of Indian sim racing teams. International organizations bring with them established best practices regarding player welfare, contract negotiations, and brand management, which Indian stakeholders are increasingly adopting. This trend is substantiated by strategic moves from global entities, such as Betsson, which expanded its partnership in Indian esports in early 2026[24]. This collaboration reflects the global appeal of Indian esports and opens doors for greater international exposure and resources for Indian players and organizations[24]. Such partnerships are pivotal because they provide the financial stability and structural rigor necessary for Indian sim racers to compete on the international stage, moving beyond the fragmented ecosystem that characterized earlier years.

Furthermore, the structure of competitive events in India is being reshaped by the global calendar. The presence of established major tournaments and competitive calendars at the international level has necessitated a restructuring of the Indian scene, specifically regarding the shaping of local event structures and their integration into global qualifiers. Historically, initiatives like KRAFTON India’s college esports tours in 2022 helped build grassroots-level engagement domestically[23]. However, the focus in 2026 has shifted from purely domestic grassroots activation to creating pathways for international prowess. Discussions among Indian esports stakeholders in January 2026 revolved around progressing from policy frameworks into actionable outcomes, focusing on creating a robust esports pipeline and enhancing talent development[25]. This shift aims to position India more prominently on the international esports stage, ensuring that Indian tournaments are not isolated events but rather recognized steps within the global championship hierarchy.

Technological advancements continue to act as a bridge between the Indian user base and the global community. Advancements in realistic driving physics and professional driver training integration, which were gaining traction globally in previous years, have now become standard expectations within the Indian community[23]. The ability of Indian platforms to host high-latency free, high-fidelity races is crucial for connecting local talent with global servers. As international developers push the boundaries of simulation software, Indian sim racers are compelled to upgrade their systems and skills to remain competitive. This dynamic ensures that the Indian scene does not stagnate; rather, it is in a constant state of modernization and adoption of new technologies, driven by the relentless pace of global innovation.

Despite the lack of granular data quantifying the exact number of active competitive sim racers in India in February 2026, the qualitative indicators of growth are robust. The convergence of official government recognition, international corporate investment, and the adoption of global competitive standards suggests that India is rapidly transitioning from a peripheral market to a significant regional hub in the global sim racing landscape. The symbiotic relationship is clear: global trends provide the technological and structural blueprint, while domestic policy reforms provide the fertile ground for these trends to take root. As esports continues to widen participation and attract a larger viewer base globally, it is expected to play an integral role in India’s market[23][25]. The narrative of Indian sim racing in 2026 is therefore one of integration and professionalization, driven by a desire to leverage global advancements to unlock local potential. The efforts to foster partnerships with global organizations aim to position India more prominently on the international esports stage, signaling a promising trajectory for the future[25].

| Influence Factor | Global Trend Overview | Impact on Indian Sim Racing Scene |

| International Events | Established major tournaments and competitive calendars | Shaping of local event structures and integration into global qualifiers |

| Technological Advancements | Rapid innovation in simulation hardware and software | Modernization of Indian racing practices and adoption of new technologies |

| Esports Organizations | Dominance of mature global esports entities | Influence on the formation and management of Indian sim racing teams |

Infrastructure and Ecosystem Development

Accessibility of Sim Racing Hardware and Software in India

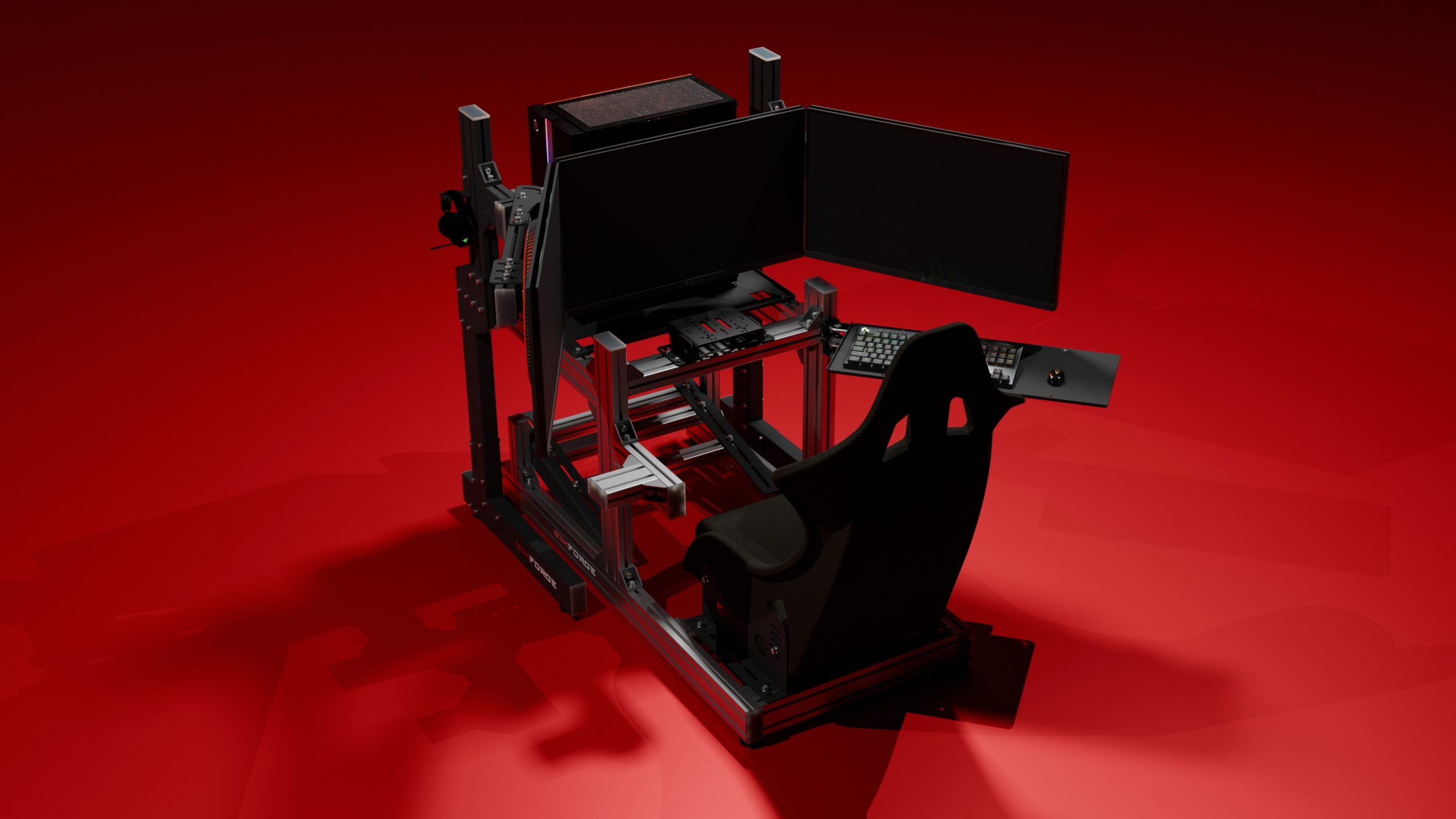

The assessment of sim racing infrastructure within India necessitates a dual analysis of physical hardware availability and the digital software ecosystem. As of February 2026, the landscape for acquiring sim racing equipment in India presents a complex scenario characterized by a dichotomy between global technological advancements and local market opacity. While the global industry continues to innovate with high-fidelity peripherals and next-generation processing units, the direct accessibility of these components for the Indian consumer remains fraught with logistical challenges and information gaps.

In the domain of hardware distribution, the market is heavily influenced by the presence—or notable absence—of established international manufacturers. As of early 2026, reports on the availability of specialized sim racing hardware in India are inconclusive due to a lack of region-specific data. Global developments, such as those showcased at CES 2026, highlight significant strides by brands like Sim Lab and SimRev, alongside the expansion of the Gran Turismo World Series; however, these industry milestones are reported without specific reference to stock allocation or retail presence in the Indian market[31]. Consequently, Indian enthusiasts often face uncertainty regarding the procurement of the latest wheel bases, pedals, and cockpits. For instance, major manufacturers like Fanatec display backorder statuses for products with shipping windows in early 2026 on their global portals, yet there is no confirmation of dedicated distribution channels or localized storefronts that would facilitate easier access for buyers in India[35]. This absence of localized support forces consumers to rely on general electronics retailers or unauthorized distributors, often resulting in inflated costs and warranty concerns.

The computational foundation required to run modern simulation software also presents a mixed picture of accessibility. Constructing a dedicated sim racing rig requires robust processing power, typically involving technologies such as Intel’s 14th generation CPUs and NVIDIA’s 40 series GPUs. While these components are generally available in the global marketplace, the specific supply chain dynamics for high-performance PC builds within India are not explicitly detailed in current industry analyses[34]. Furthermore, forward-looking technologies like Intel’s Nova Lake architecture are anticipated to influence next-generation simulation fidelity, but their relevance to the immediate Indian retail landscape remains speculative and theoretical rather than practical[32].

A critical factor defining the accessibility of this ecosystem is affordability. The financial outlay required to participate in sim racing in India varies drastically depending on the level of immersion sought by the user. An analysis of hardware tiers reveals a stark cost progression. For an entry-level setup, typically consisting of a gear-driven wheel and standard pedals, the average cost is estimated at approximately 35,000.0 INR. This price point represents the most accessible tier for newcomers. However, as enthusiasts seek higher fidelity, the costs escalate significantly. Moving towards professional-grade equipment, which includes high-torque Direct Drive (DD) bases, load cell pedals, and structural rigs, the financial commitment increases substantially. Market data indicates that such high-end configurations can reach an estimated maximum value of 450,000.0 INR. This wide range, from 35,000.0 INR to 450,000.0 INR, underscores an increasing trend in cost that correlates directly with hardware complexity and performance, potentially limiting the upper echelons of the hobby to a niche demographic.

On the software front, the ecosystem is shaped less by physical retail and more by the regulatory and digital infrastructure frameworks established by the government. As of February 2026, detailed reports on the distribution of sim racing software titles via digital storefronts or SaaS platforms in India are limited. However, broader macroeconomic policies are creating an environment conducive to digital growth. The Union Budget 2026-27 has introduced measures to streamline the IT sector, including an increase in the safe harbour threshold for IT companies to INR 2,000 crore and the consolidation of IT-related services into a single category[34][35]. These regulatory adjustments aim to enhance operational efficiency for technology firms, which could indirectly improve the stability and speed of software distribution networks. Additionally, the government’s focus on fostering a high-tech ecosystem through incentives for cloud and AI data centers suggests a prioritization of digital infrastructure that is vital for downloading large simulation titles and maintaining low-latency connections for online racing[33].

Despite these positive structural indicators, there remains a lack of specific intelligence regarding software licensing and distribution trends unique to the Indian sim racing market. Older reports regarding AI chip advancements or regulatory audits by TRAI do not offer immediate insights into how racing simulations are marketed or sold to Indian users[31][32]. The reliance on cloud technology and the strengthening of the semiconductor industry are promising for the long-term viability of software access, yet they do not address current consumer questions regarding localized pricing or server availability[33].

Ultimately, the accessibility of sim racing in India is currently defined by a heavy reliance on self-conducted research and community knowledge. Due to the rapid evolution of the industry and the lack of up-to-date, India-specific commercial reports, potential consumers often resort to browsing localized forums and communities to gauge stock levels and software compatibility, as older discussions from late 2023 are no longer reliable indicators of the current market[33]. The gap between global availability and local accessibility highlights the need for dedicated distribution networks that can bridge the divide between international manufacturers and the growing Indian sim racing community

Role of Gaming Communities and Esports Organizations

The development of the sim racing ecosystem in India as of February 2026 is fundamentally anchored in the synergistic relationship between grassroots gaming communities and formalized esports organizations. This dynamic interaction has been pivotal in transitioning sim racing from a solitary hobbyist pursuit into a structured competitive discipline. The architecture of this ecosystem is defined by distinct roles: gaming communities act as the primary drivers of participation and infrastructure accessibility, while esports organizations and global entities provide the necessary competitive frameworks, league structures, and pathways for international integration. This collaborative progression is evident in the proliferation of physical infrastructure, the establishment of national-level championships, and the increasing professionalization of the sector, which mirrors the broader trajectory of the Indian esports industry.

At the foundational level, gaming communities have been instrumental in addressing the inherent barriers to entry within sim racing, particularly regarding the high cost of hardware and simulation equipment. Community-driven initiatives have focused on building networks that foster engagement and resource sharing. Indicators from social platforms such as Reddit, specifically within the r/SimracersIndia community, suggest that Indian sim racers have actively worked to build communities that foster league racing and expand access to related infrastructure[45]. A critical development in this regard has been the establishment of physical access points, such as the opening of new centers in Bangalore as of late 2024. These centers serve as hubs where enthusiasts can access high-fidelity equipment without the need for prohibitive personal investment, thereby democratizing access to the sport. The efficacy of these community efforts is further reflected in the grassroots competitive scene. For instance, COMP-EX 2026 hosted a sim racing event in Bangalore featuring an F1 Time Trial format with a modest prize pool, reflecting the grassroots yet competitive nature of such gatherings[14]. These events, while local in scale, are vital for sustaining community participation and identifying emerging talent outside of the professional league circuit.

Ascending the ecosystem hierarchy, esports organizations have assumed the role of developing competitive infrastructure and formalizing the sport through the establishment of leagues and championships. The operational capacity of these organizations to execute large-scale events was notably demonstrated during the ESGF Esports National Championship 2026. This event marked a notable milestone for sim racing in the country, showcasing motorsport simulation titles like Gran Turismo 7 and featuring Rahul Alvah as its Central Zone winner[41]. The inclusion of specific titles like Gran Turismo 7 in national rosters highlights the increasing integration of sim racing into esports competitions[41]. Unlike the fragmented nature of community time trials, these organizational initiatives provide a standardized regulatory environment, ensuring that Indian sim racing aligns with competitive norms. However, despite these advancements, the scene remains a niche within the broader gaming landscape. Events unrelated to sim racing, such as the EAFC 26 Ultimate Showdown at Immortal Gaming Cafe, Delhi, reflect the vibrant but diverse competitive gaming landscape in India, suggesting that sim racing occupies only a small portion of the overall esports domain[43].

The growth of sim racing is also deeply influenced by the macro-developments within the wider Indian esports sector, where major organizations are actively shaping policy and talent development pipelines. The push for legitimacy has reached the highest levels of governance, with strong efforts from the gaming industry to push for official recognition of esports as a sport in India, leading to discussions around this being included in the country’s Budget 2026 announcement[41]. Such recognition is crucial for niche disciplines like sim racing, as it facilitates sponsorship acquisition and institutional support. Furthermore, the strategies employed by major entities like KRAFTON India serve as a blueprint for ecosystem development that sim racing organizations are beginning to emulate. KRAFTON India has notably contributed to the grassroots development of esports with initiatives like a nationwide college campus tour involving 128 colleges across various city tiers[42]. This extensive outreach aims to identify talent, develop skills, and foster sustainable competitive environments, offering a clear insight into how organizations actively work to embed esports in academic and societal frameworks[42]. Additionally, KRAFTON India’s 2026 esports roadmap, unveiled in November 2025, aims to establish a structured pathway for players to progress from grassroots participation to global competition[43]. This structured approach creates a trickle-down effect, where the professional standards, coaching methodologies, and management practices established for mainstream titles gradually permeate the sim racing sector.

The professionalization of the ecosystem is further evidenced by the economic opportunities emerging for participants and support staff. Organizations are instrumental in professionalizing the esports landscape by scouting talent, organizing tournaments, securing sponsorships, and managing careers[45]. This systemic evolution has contributed to an increasing number of players viewing esports as a viable career option, with top players reportedly earning up to Rs 1 crore annually as of early 2024[45]. While these figures largely represent the upper echelon of mainstream esports athletes, the trend has opened up new opportunities for coaches and managerial roles essential for sustaining a structured industry environment. As sim racing leagues grow in stature, the demand for specialized technical coaches and telemetry analysts is expected to rise, following the trajectory set by established esports genres.

Finally, the role of global entities and international integration remains a critical component of the ecosystem’s maturity. The integration of Indian esports into the global market is accelerating, indicated by strategic partnerships such as Betsson’s collaboration to strengthen its presence in India’s sports and esports sectors as of January 2026[14]. This indicates growing collaboration within the global gaming ecosystem and suggests that international stakeholders view the Indian market as a viable investment frontier[14]. However, the sector must remain vigilant regarding the quality of this integration. Broader critiques of sim racing’s global ecosystem, including its limited appeal and insular nature, as expressed in 2023, might also resonate within the niche Indian scene, where expanding accessibility and interest remains a challenge[42]. To mitigate this, Indian organizations must balance high-level competitive integrity with broad-based community engagement.

In conclusion, the infrastructure and ecosystem development of sim racing in India in early 2026 is characterized by a dual-engine growth model. On one side, gaming communities are expanding physical access and sustaining grassroots enthusiasm through local events and centers. On the other, esports organizations are formalizing the competitive landscape through national championships and aligning the sector with broader industry advancements in recognition, professionalization, and talent development. While data gaps exist regarding the specific long-term sustainability of recent initiatives, the convergence of community passion and organizational strategy suggests a developing, albeit niche, ecosystem poised for further integration into the global sim racing domain.

| Stakeholder Type | Role in Ecosystem | Key Initiatives |

| Gaming Communities | Building the sim racing ecosystem | Community-driven initiatives |

| Esports Organizations | Developing competitive infrastructure | Establishment of leagues |

| Global Entities | International integration | Collaborations with global esports entities |

Indian Motorsport Integration and Manufacturer Involvement

The development of infrastructure and the broader ecosystem for sim racing in India represents a complex intersection of digital acceleration, evolving motorsport interest, and sporadic capital investment. As of February 2026, the landscape is defined by a transition from nascent, enthusiast-driven pockets of activity to a more structured, albeit geographically fragmented, industry. The trajectory of this sector is heavily influenced by the general state of Indian motorsport, the availability of high-performance hardware, and the strategic positioning of manufacturers who view simulation not merely as entertainment, but as a crucial entry point into the racing vertical.

The physical infrastructure supporting sim racing in India has witnessed discernible growth, reflecting the global rise of esports and motorsport-related gaming technologies. Between 2020 and 2023, the primary focus area for infrastructure investment was the setup of dedicated facilities, characterized by increased capital flow into the sector. A prominent example of this trend was the launch of a new sim racing center in Bangalore’s HSR Layout in November 2023[53]. This development serves as a critical case study of localized infrastructure development, offering high-fidelity equipment to a consumer base that may not have the financial capacity to own professional-grade rigs at home. However, while such centers illustrate the potential for a commercial sim racing model, the operational status and subsequent long-term impact of these early facilities remain difficult to quantify comprehensively due to limited publicly available data as of early 2026[53]. The available information suggests that these establishments represent isolated developments rather than a systematic, nationwide growth in infrastructure.

Parallel to physical venues, the ecosystem is underpinned by technological progress, specifically the adoption of advanced simulation hardware and software. The global context provides a favorable backdrop for this adoption; for instance, the market for high-performance sim racing pedals is projected to experience a compound annual growth rate of 11.1% from 2026 to 2033[54]. While specific references to India’s domestic adoption within this market segment are not explicitly detailed, the global expansion points to hardware innovations and growing consumer demand that inevitably permeate the Indian market[54]. Furthermore, India’s broader technological environment has matured significantly. The country’s leadership in 5G implementation and fiscal initiatives designed to attract AI workloads through tax incentives have created a robust digital backbone[41]. Although these advancements in digital connectivity and technical innovation are not directly linked to sim racing in the analyzed sources, they indirectly bolster the sector by ensuring the low-latency connectivity and processing power required for competitive online racing and complex physics simulations[41].

The integration of sim racing into the wider Indian motorsport fabric involves complex dynamics between virtual platforms and traditional racing entities. The motorsport ecosystem in India between 2020 and 2023 showcased a developing yet uneven trajectory, influenced by infrastructural challenges and engagement gaps. During this period, the key trend in ecosystem integration was the pursuit of strategic partnerships bridging virtual and real racing. By February 2026, this integration had become more visible, with motorsport events hosted in India including professional-grade racing simulators among their attractions[55]. This inclusion signifies a shift where simulation is no longer viewed solely as a peripheral activity but as a central component of fan engagement and motorsport development. However, the presence of simulators at events does not directly confirm the existence of a widespread or established sim racing infrastructure across the country, indicating that the bridge between the virtual and physical tracks is still under construction[55].

Stakeholder engagement remains a critical variable in this ecosystem. Between 2020 and 2023, the trend was characterized by active participation in fostering the racing ecosystem, primarily driven by Indian motorsport entities and manufacturers. However, this period was also fraught with barriers that stifled consistent progress. Despite genuine attempts to promote motorsport, the lack of consistent high-skill pathways for aspiring professionals was a persistent concern[52]. Regional aspirations occasionally provided necessary momentum; for example, areas such as Goa demonstrated grassroots vigor, with enthusiasts and local stakeholders like Chrys D’souza working toward energizing the rally racing scene[53]. While these efforts were specific to physical rallying, they contributed to the broader racing culture essential for a thriving sim racing community. Conversely, at the national level, ambition often outpaced execution. The government’s interest in reviving Formula 1 at the Buddh International Circuit (BIC) was a central theme, involving visits and exploratory discussions, yet concrete progress remained ambiguous due to financial and bureaucratic hurdles. This historical context highlights the challenges manufacturers and large entities face when attempting to establish a cohesive national framework for racing, whether virtual or physical.

The role of manufacturers and corporate entities in this ecosystem is evolving from passive sponsorship to active infrastructure development. The primary focus areas for these stakeholders have shifted toward collaboration opportunities that leverage the relatively lower barrier to entry of sim racing to identify talent. However, the ecosystem remains constrained by the lack of fully up-to-date and comprehensive data, leaving gaps in understanding the overall state of sim racing infrastructure in the country as of 2026[55]. The narrative derived from available sources reflects a sector where individual developments—such as the Bangalore center or the inclusion of simulators in 2026 events—showcase growing participation, yet fail to present a unified picture of a mature industry.

Ultimately, the state of sim racing infrastructure in India is one of potential intertwined with structural limitations. The years 2020 through 2023 served as a foundational period where the limitations of the traditional motorsport ecosystem—such as the high cost of participation and lack of tracks—highlighted the necessity for digital alternatives[52]. The subsequent years have seen the slow crystallization of these alternatives through isolated investments and technological upgrades. While the global hardware market expands and India’s digital grid strengthens, the translation of these advantages into a widespread, accessible, and professionalized sim racing ecosystem is an ongoing process. The evidence points to a period of measured and incremental advancement rather than transformative growth, with the future trajectory dependent on whether isolated success stories can be replicated into a national network of training facilities and competitive leagues[52].

| Development Aspect | Key Trends (2020-2023) | Primary Focus Areas |

| Infrastructure Investment | Increased capital flow into sim racing facilities | Key Investments & Facility Setup |

| Technological Progress | Adoption of advanced simulation hardware/software | Technological Advancements |

| Ecosystem Integration | Strategic partnerships bridging virtual and real racing | Collaboration Opportunities |

| Stakeholder Engagement | Active participation in fostering the racing ecosystem | Indian Motorsport Entities & Manufacturers |

Opportunities, Challenges, and Future Prospects

Rising Popularity Among Indian Gamers and Motorsport Enthusiasts

The trajectory of sim racing in India has witnessed a profound evolution, mirroring the broader expansion of the national gaming and esports ecosystem. While the global narrative surrounding sim racing suggests a steady rise in the racing simulator market—projected to grow from 0.93 billion USD in 2025 to 1.01 billion USD in 2026—the Indian context presents a unique convergence of demographic shifts, technological accessibility, and evolving cultural acceptance of gaming as a legitimate pursuit[15]. As of 2025, the Indian gaming market was valued at 4.38 billion USD, with projections indicating a rise to 5.02 billion USD in 2026 and a potential surge to 9.89 billion USD by 2031, providing a fertile economic backdrop for niche genres like sim racing to flourish[65].

Analysis of the enthusiast base in India reveals a compelling story of rapid adoption and community expansion. Between 2020 and 2023, the number of sim racing enthusiasts in the country quadrupled. Starting from an estimated base of 50,000 individuals in 2020, the community expanded to 90,000 in 2021, grew further to 140,000 in 2022, and reached 200,000 by the end of 2023. This exponential growth aligns with global trends observed during the early months of 2020, where the genre experienced a significant surge driven by pandemic-induced lockdowns. Globally, this period saw a 117 percent increase in live-viewing hours on platforms such as Twitch and YouTube between February and April 2020, a momentum that catalyzed interest among Indian users who sought digital alternatives to real-world motorsport and outdoor entertainment[65].

A granular examination of the demographics driving this popularity highlights a distinct shift toward a younger, digital-native audience. In 2020, the 16-24 age group constituted 40 percent of the Indian sim racing enthusiast base. By 2023, this cohort had grown to represent 45 percent of the total demographic, signaling that sim racing is increasingly resonating with students and young professionals. Conversely, the 25-34 age bracket, while still significant, saw a marginal decline in proportional representation, dropping from 45 percent in 2020 to 42 percent in 2023. The 35-plus age group also witnessed a slight decrease in its share, moving from 15 percent to 13 percent over the same period. These shifts suggest that while the genre retains its appeal among mature audiences, the influx of new entrants is predominantly skewed toward younger gamers, likely influenced by the proliferation of accessible gaming hardware and the integration of racing titles into popular culture.

Furthermore, the primary background of these enthusiasts has undergone a transformation that underscores the genre’s crossover appeal. Historically viewed as a training ground for motorsport aspirants, sim racing in India is increasingly becoming a domain for general gamers. In 2020, 60 percent of the enthusiast base identified primarily as gamers, while 40 percent identified as motorsport enthusiasts. By 2023, the share of those identifying primarily as gamers had risen to 65 percent, reducing the motorsport enthusiast segment to 35 percent. This trend indicates that sim racing is successfully breaking out of its niche silo and establishing itself as a mainstream genre within the broader gaming industry. This evolution is partly supported by the market’s shift toward providing engaging mid-range gaming experiences that cater to a cost-conscious demographic, a trend noted in historical contexts regarding monetization strategies and Average Revenue Per Paying User (ARPPU) increases[64].

Geographically, the adoption of sim racing is no longer confined to India’s metropolitan hubs. While Tier 1 cities continue to dominate the landscape, their share of the enthusiast base has seen a gradual decline, falling from 75 percent in 2020 to 70 percent in 2023. In contrast, Tier 2 and 3 cities have demonstrated a steady uptake, with their contribution rising from 25 percent in 2020 to 30 percent in 2023. This decentralization of the user base can be attributed to increased internet accessibility and smartphone penetration, which have been pivotal in propelling the industry’s development across the country. Mobile gaming remains a crucial area of growth in these regions, serving as a gateway for users who may eventually transition to more dedicated sim racing hardware setups.

The rising popularity of sim racing also coincides with a critical period of formalization and policy advocacy within the Indian gaming sector. The industry is navigating a shift toward greater legitimacy, exemplified by initiatives such as PROGA 2025, which marked a pivotal moment for the recognition of gaming and esports in the country[11]. Stakeholders are actively advocating for government support, seeking tax parity with other entertainment sectors, increased funding for intellectual property (IP) development, and incentives to promote gaming exports[53]. These efforts are designed to foster indigenous game development and reduce reliance on foreign IP, a move that could eventually lead to the creation of India-centric racing simulators or tracks, further boosting local engagement[53].

However, this growth trajectory is not without its societal and regulatory challenges. The expansion of the user base has drawn attention to potential negative externalities. Concerns highlighted in the 2026 Economic Survey regarding digital addiction, particularly through the overuse of gaming and social media, suggest that societal impacts may affect future perceptions of gaming adoption and usage in India[15]. As the number of enthusiasts hits the 200,000 mark and beyond, the industry must balance its commercial expansion with responsible gaming practices to maintain public trust and regulatory support.

Despite these challenges, the future prospects for sim racing in India appear robust. The increasing alignment of the “gamer” identity with sim racing, coupled with the geographic deepening of the market into Tier 2 and Tier 3 cities, creates a diverse and resilient ecosystem. While localized data on specific hardware adoption remains limited, global analyses emphasize future growth trends in high-performance pedals and racing simulator hardware, suggesting that the Indian market will likely see an influx of advanced equipment as the enthusiast base matures[53]. The “65” further highlights growth drivers in this niche, reinforcing the view that the sector is poised for long-term expansion[64]. As the market heads toward the projected 9.89 billion USD valuation by 2031, sim racing stands as a significant vertical capable of bridging the gap between virtual entertainment and professional motorsport, driven by a young, enthusiastic, and increasingly widespread demographic[65].

| Characteristic | Metric | 2020 | 2021 | 2022 | 2023 |

| Total User Base | Number of Enthusiasts (Estimated) | 50,000 | 90,000 | 140,000 | 200,000 |

| Age Distribution | 16-24 Years (%) | 40 | 42 | 44 | 45 |

| — | 25-34 Years (%) | 45 | 44 | 43 | 42 |

| — | 35+ Years (%) | 15 | 14 | 13 | 13 |

| Primary Background | Gamer (%) | 60 | 62 | 64 | 65 |

| — | Motorsport Enthusiast (%) | 40 | 38 | 36 | 35 |

| Geographic Spread | Tier 1 Cities (%) | 75 | 73 | 71 | 70 |

| — | Tier 2 & 3 Cities (%) | 25 | 27 | 29 | 30 |

Challenges in Adoption: Cost, Awareness, and Accessibility

The trajectory of simulation racing (sim racing) in India presents a complex dichotomy between global technological acceleration and local structural inertia. While the digitization of motorsport gained unprecedented momentum globally between 2020 and 2023, largely catalyzed by the constraints of the pandemic, the Indian context revealed deep-seated impediments to widespread adoption. The integration of sim racing into the country’s sporting ecosystem has been significantly hindered by an underdeveloped motorsport infrastructure and a persistent lack of institutional support[74]. Unlike in Western markets where virtual racing acts as a recognized parallel or feeder discipline to track racing, the absence of well-established pathways in traditional motorsport in India has created a vacuum. Without these foundational structures, allied sectors such as sim racing have struggled to secure necessary recognition, sponsorship, and investment, thereby limiting the opportunities available to enthusiasts during this formative period[74].

Foremost among the challenges stifling the growth of this sector is the economic barrier to entry, specifically regarding the acquisition of necessary equipment. Quantitative analysis of the major barriers to sim racing adoption in India during the 2020–2023 period indicates that “High Hardware & Setup Costs” constituted the single most significant obstacle, accounting for a commanding 50.0% of the challenges faced by potential adopters. This financial hurdle is corroborated by industry reports from February 2024, which noted that even basic racing simulator hardware, comprising essential components such as steering wheels, pedal sets, and metal frames, was typically priced below USD 2,000[54]. While this price point might be considered accessible in high-income economies, it represents a substantial capital investment for the average Indian consumer, particularly when juxtaposed against the costs of traditional gaming or other recreational sports. Furthermore, while the global racing simulator market has been projected to witness robust expansion—with estimates suggesting a value of USD 2.04 billion by 2030 at a Compound Annual Growth Rate (CAGR) of 15.78%—these figures reflect a global outlook and do not account for the specific purchasing power parity or import duty structures prevalent in the Indian market[71]. Consequently, the high cost of entry has restricted participation to a niche demographic, preventing the sport from achieving critical mass.

The economic challenges are compounded by issues of accessibility and supply chain limitations. Although sim racing hardware has seen steady growth globally, with projections indicating a CAGR of 12-15%, the availability of high-quality rigs and peripherals in India has remained inconsistent[75]. The Indian scenario implies potentially higher entry costs due to factors such as import taxes and limited local production, which exacerbate the financial burden on the consumer. The lack of a robust domestic manufacturing base for sim racing peripherals means that enthusiasts are often reliant on expensive imports, further widening the gap between interest and participation. In contrast to the overarching financial hurdles, “Other Technical Challenges” represented a minimal portion of the barriers, accounting for only 5.0% of the impediments during the analyzed period. This disparity suggests that the primary friction is not technological illiteracy or software complexity, but rather the brute financial capability to acquire the requisite hardware.

Beyond the tangible barriers of cost and equipment lies the intangible, yet equally pervasive, challenge of awareness and cultural acceptance. There has been a notable lack of public awareness and mainstream acceptance of sim racing as a legitimate form of motorsport in India[73]. Culturally, the activity is frequently conflated with casual gaming rather than being recognized as a disciplined competitive sport or a valid training ground for professional racing. This perception gap, combined with a smaller base of gamers and racers compared to Western counterparts, has significantly slowed the industry’s growth trajectory. Initiatives to bridge this gap have been sporadic and often misaligned with the broader goal of fostering a cohesive industry. For instance, events like Formula Bharat showcased interest in the technical simulation aspects of the field; however, these efforts remained disjointed and were primarily focused on engineering competitions rather than fostering sim racing as an organized, spectator-friendly industry[73]. Consequently, while such platforms provided a venue for technical engagement, they did not effectively translate into mainstream popularity or commercial viability for sim racing as a sport.

The ecosystem’s stagnation is also attributable to the broader struggles of the Indian motorsport sector. As highlighted in reports discussing motorsport challenges, the absence of a thriving real-world racing economy deprives sim racing of its natural commercial partner[74]. In developed markets, sim racing often benefits from the trickle-down economics of Formula 1, GT racing, and touring car championships. In India, where these sectors are still maturing, sim racing is left to fend for itself without the safety net of established sponsorship networks or career development programs. Global tournaments have offered some online opportunities for Indian talent, but local infrastructure deficits have hampered the country’s competitive presence on the international stage. The lack of organized local events and high-quality training facilities means that even talented Indian sim racers struggle to bridge the gap to professional competition.

Despite these multifaceted challenges, the period between 2020 and 2023 was not without merit. The groundwork laid during these years helped maintain a foothold for sim racing, marking it as an area with potential for future development as India’s motorsport ecosystem matures. The global market context remains promising, with the industry size expected to grow from USD 0.93 billion in 2025 to USD 1.01 billion in 2026. However, this global optimism must be tempered with regional realism. As of February 2026, there remains insufficient direct evidence to confirm whether the specific cost and infrastructure barriers identified in the earlier part of the decade have been effectively resolved. While global trends suggest market expansion, the regional adaptations required to address the cost barriers in India—such as localization of manufacturing or tariff adjustments—remain complex and largely undocumented in recent literature. The persistence of high costs, coupled with the need for greater institutional recognition, suggests that while the “virtual” nature of the sport offers theoretical accessibility, the “physical” reality of economic and structural limitations continues to define the adoption curve in India.

Potential for Growth: Esports Tournaments, Sponsorships, and Training Platforms

The trajectory of sim racing in India has shifted from a fragmented, enthusiast-driven pursuit into a structured component of the broader motorsport and esports landscape. This evolution offers distinct opportunities for stakeholders to capitalize on a growing competitive ecosystem, particularly through the expansion of esports tournaments, the cultivation of sponsorship frameworks, and the establishment of dedicated training platforms. As of February 2026, the sector demonstrates a level of maturity that was only aspirational in previous years, yet the historical data from the formative period of 2020 to 2023 provides the critical baseline for understanding current growth potential.

The expansion of esports tournaments serves as the primary engine for this sector’s development. Quantitative analysis of the ecosystem reveals a consistent upward trend in tournament frequency and professionalization. In 2020, the estimated number of major sim racing tournaments in India stood at approximately eight, a figure largely driven by a pandemic-induced surge in online participation and the impromptu establishment of community leagues. This period was characterized by high engagement but low institutional structure. However, by 2021, the landscape began to shift as the number of major tournaments nearly doubled to fifteen. This growth was catalyzed by the formal recognition of the discipline by the Federation of Motor Sports Clubs of India (FMSCI) and the introduction of National Digital Cups, which provided a semblance of regulatory oversight and competitive legitimacy. The momentum continued into 2022, where the estimated tournament count rose to twenty-five, coincided with the entry of corporate sponsorships and the launch of talent identification initiatives such as the ‘Indian Racing League’. By 2023, the ecosystem had expanded further to host forty major tournaments, driven by the proliferation of dedicated training platforms and the deepening integration of sim racing with real-world motorsport pathways.

Despite this clear statistical growth, the historical documentation of specific events during the 2020 to 2023 distinct timeframe remains fragmented. While the esports scene sought to formalize the domain by 2023, comprehensive evaluative accounts of this evolution are sparse, often limited to promotional snippets rather than retrospective analysis. A pivotal development in this era was the introduction of India’s first National Esports GT3 Championship, which was designed to establish a premier competitive platform for sim racers within the country[43]. This championship, which featured qualifiers commencing in late February 2023, represented a significant step toward standardization, offering Indian sim racers a national platform to compete in both sprint and endurance formats[43][3]. However, the specific lineage of such championships remains somewhat ambiguous, with insufficient data available to directly link these formalized events to the ad-hoc tournaments held in 2020 and 2021[3]. The recurring mention of “first-ever” championships during this period implies a delayed establishment of centralized governance, suggesting that while the volume of events increased as per the ecosystem data, the consolidation of these events into a unified historical record was challenging[83][43]. Consequently, while the momentum was undeniable, the archival evidence from 2020 to 2023 serves more as an indicative summary of growth rather than a detailed registry of every competitive event.

Parallel to the rise of tournaments is the critical, yet complex, arena of sponsorship. For the ecosystem to sustain the trajectory seen between 2020 and 2023, transitioning from community funding to corporate sponsorship is essential. As of early 2026, the search for dedicated sim racing sponsorships in India often uncovers a landscape heavily skewed toward physical motorsport and engineering competitions rather than pure virtual racing. For instance, entities like CADFEM India have historically supported initiatives such as Formula Bharat, with engagement tracing back to 2016[81]. Similarly, technology providers like Ansys have participated in events such as the Simulation Challenge for Formula Bharat 2026[43]. While these examples highlight a corporate willingness to invest in simulation technology and automotive engineering, they primarily function as technology facilitators for student-run engineering teams rather than direct financial sponsors for professional sim racing leagues[43].

The sponsorship challenges are further illuminated by the nature of available resources, which often conflate virtual racing with physical track management or student engineering projects. Information regarding the Global Motorsport Venue Summit & Awards, for example, focuses on physical infrastructure and venue management in Qatar, lacking direct relevance to the virtual racing economy[43]. Furthermore, sponsorship solicitations from groups such as Team Kratos Racing typically target funding for composite Formula Student vehicles, reinforcing the industry’s historical preference for tangible motorsport assets over virtual platforms[83]. This disconnect highlights a substantial market gap and a subsequent opportunity. The existing support for engineering simulation by major tech firms suggests that the foundational interest in virtual testing and competition exists. The strategic imperative for the future is to convert these technology partners—who already support events like Formula Bharat—into active sponsors of sim racing tournaments by demonstrating the overlap between high-fidelity simulation and esports audience engagement[3].

To bridge the gap between tournament frequency and commercial viability, the establishment of training platforms has emerged as a vital third pillar of growth. The data indicates that by 2023, the proliferation of such platforms was a key driver in expanding the tournament scene to forty major events. These platforms are not merely software interfaces but ecosystem enablers that facilitate the transition from amateur gaming to professional competition. The “Indian Racing League” talent hunt programs, introduced around 2022, exemplify the potential of these platforms to serve as conduits for talent development, effectively democratizing access to motorsport. By providing structured training environments, these platforms enhance the competitive quality of the tournaments, thereby making the ecosystem more attractive to the aforementioned hesitant sponsors.

In conclusion, the potential for growth in Indian sim racing is underpinned by a demonstrably expanding tournament calendar and the nascent infrastructure of training platforms. The journey from eight tournaments in 2020 to forty in 2023 illustrates a robust demand for competitive play. However, realizing the full future prospects of this sector requires addressing the historical fragmentation of the ecosystem and converting tangential engineering sponsorships into direct esports investment. The path forward involves leveraging the rigorous simulation technologies already present in the Indian market to legitimize sim racing not just as a game, but as a verified sub-discipline of motorsport.

| Year | Estimated Number of Major Sim Racing Tournaments | Key Growth Drivers & Milestones |

| 2020 | 8 | Pandemic-induced surge in online participation; Establishment of community leagues |

| 2021 | 15 | Recognition by FMSCI (Federation of Motor Sports Clubs of India); Introduction of National Digital Cups |

| 2022 | 25 | Corporate sponsorships enter the ecosystem; Launch of talent hunt programs like ‘Indian Racing League’ |

| 2023 | 40 | Proliferation of dedicated training platforms; Integration of sim racing with real-world motorsport paths |

References

[1] Round-up: Indian government ‘working to bring F1 back’ https://www.racefans.net/2026/02/04/round-up-4th-february-2026/

[2] 🏁 2026 PRO SPEC SIM TOURNAMENT 🏁 The official MultiGP esports competition https://www.facebook.com/MultiGPDroneRacing/posts/-2026-pro-spec-sim-tournament-the-official-multigp-esports-competition-is-live-r/1273847854770484/

[3] India’s first National Esports GT3 Championship is finally here https://www.instagram.com/reel/DUQjxoziU59/

[4] Generation Speed – India’s premier motoring festival returns https://machineedgeglobal.com/2026/01/14/generation-speed-indias-premier-motoring-festival-returns-for-its-second-edition-on-7th-8th-february-2026-at-aamby-valley/

[5] Govt explores return of F1 races to India https://timesofindia.indiatimes.com/sports/racing/top-stories/govt-explores-return-of-f1-races-to-india/articleshow/127876174.cms

[6] India gaming market trends and growth opportunity (2026) https://uk.finance.yahoo.com/news/india-gaming-market-trends-growth-105800457.html

[7] Orange Economy: India ramps up animation and gaming skilling https://www.forbesindia.com/article/budget-2026/orange-economy-india-ramps-up-animation-and-gaming-skilling-push-in-budget-2026/2990967/1

[8] Budget 2026: Gaming industry welcomes AVGC labs push https://www.exchange4media.com/budget-news/budget-2026-gaming-industry-welcomes-avgc-labs-push-151537.html

[9] How Budget 2026 will help young Indians build creator careers https://thebetterindia.com/education/union-budget-2026-creator-labs-india-11067472

[10] This is where Indian esports evolves from competition https://www.instagram.com/p/DUSQTiVD6TO/

[11] Sports + Esports convergence: The rise of Sim Racing https://asiasportstech.com/portfolio/sim-racing/

[12] IndiaWin and the growing landscape of Sim Racing https://www.weareiowa.com/article/news/local/plea-agreement-reached-in-des-moines-murder-trial/524-3069d9d4-6f9b-4039-b884-1d2146bd744f

[13] Esports trends in 2026: What industry figures say https://escharts.com/news/esports-trends-2026-industry-figures-insights

[14] Where is competitive Sim Racing in 2026? https://www.youtube.com/watch?v=7lAwv6wugZw

[15] Racing Simulator market size, share & growth https://www.thebusinessresearchcompany.com/report/racing-simulator-global-market-report

[17] Streaming revenues drive esports career interest in India https://www.storyboard18.com/gaming-news/streaming-revenues-drive-esports-career-interest-stability-still-elusive-in-india-87981.htm

[19] India’s AVGC revolution 🇮🇳 2 million jobs by 2030 https://www.instagram.com/p/DUQpBHJkhT9/

[20] Esports set to explode as real-money games face ban https://www.whalesbook.com/news/English/tech/Indias-Gaming-Revolution-Esports-Set-to-Explode-as-Real-Money-Games-Face-Ban/695283ea4342f77179dcf294

[21] The HUGE changes coming to Sim Racing in 2026 https://www.youtube.com/watch?v=NznV1RXivrM

[23] Racing telemetry market size, trends & forecast https://www.coherentmarketinsights.com/industry-reports/racing-telemetry-market

[24] Emerging growth patterns driving sports expansion https://www.openpr.com/news/4378080/emerging-growth-patterns-driving-expansion-in-the-sports

[25] Sim Racing hardware market size & forecasts https://www.linkedin.com/pulse/sim-racing-hardware-market-size-share-forecasts-key-c39ac/

[26] KRAFTON India builds the future of Indian esports https://www.tribuneindia.com/news/business/krafton-india-builds-the-future-of-indian-esports-through-nationwide-128-college-campus-tour-now-in-its-second-year-2-2/

[30] Indian esports stakeholders discuss 2026 prospects https://esportsinsider.com/2026/01/indian-esports-stakeholders-discuss-2026-prospects

[31] One-stop guide for new & veteran sim racers https://www.reddit.com/r/simracing/comments/1quz55y/rsimracing_monthly_super_thread_a_onestop_guide/

[32] Best Sim Racing PCs – Buyer’s Guide 2026 https://simracingsetup.com/product-guides/best-pc-for-sim-racing/

[33] Fanatec – realistic sim racing hardware https://www.fanatec.com/us/en

[34] Next-gen hardware for Sim Racing https://boxthislap.org/next-gen-hardware-for-simracing/

[35] What CES 2026 tells us about Sim Racing’s future https://www.youtube.com/watch?v=gGQy6SjzifI

[36] Budget 2026–27 lays foundation for AI data centres https://www.pib.gov.in/PressReleseDetail.aspx?PRID=2221894®=1&lang=1

[38] Top tech trends shaping India in 2026 https://www.businessworld.in/article/top-10-tech-trends-2026-india-ai-chips-585387

[41] New Sim Racing centre opens in Bangalore https://www.reddit.com/r/SimracersIndia/comments/1quvitg/new_sim_racing_centre_in_bangaloreee/

[71] Red Bull Hot Laps 2026 https://www.redbull.com/in-en/events/red-bull-hot-laps

[86] Formula Bharat 2026 sponsors https://formulabharat.com/formula-bharat-2026/sponsors/

[89] Global Motorsport Venue Summit & Awards – Doha https://www.linkedin.com/posts/circuitsummit_circuit-the-global-race-track-summit-activity-7389636796684374016-J6aH

Leave a Reply